Time once again for a list of compelling stock ideas for the new year courtesy of our all-star roster of eight money managers, analysts and investment newsletter writers.

From real estate expert Dennis Mitchell doubling down on a large cap stock to Davis Rea Investment Analyst Matthew Aspro’s favourite U.S. bank to market-beating contrarian Benj Gallander, who won last year’s stock picking challenge with a gain of 40 per cent.

From large caps to small, dividend payers to growth companies and turnaround stories, we’ve assembled an eclectic array of top stock picks for you to consider to freshen up your portfolio.

**

Benj Gallander, President, Contra The Heard Investment Letter

Fuel Tech (NASDAQ: FTEK)

Fuel Tech works in the water treatment field for utilities and industrial applications.

It also optimizes combustion systems and emissions control.

After years of losing money, it is operating around the break-even level.

It has a beautiful balance sheet, with cash and cash equivalents of $24.1 million and zero debt, while trading below book value.

The initial sell target is $4.84.

**

Ryan Modesto, Portfolio Manager, i2i Long/Short US Equity Fund

Crocs Inc. (NASDAQ:CROX):

Whether it is the valuation at roughly 9.5X forward earnings, expected revenue growth at 11 per cent for 2023, or a potential catalyst as debt is paid down and the company potentially reinstates share repurchases, we think CROX offers something to like for all types of investors.

Meanwhile, CROX has transformed itself from the ‘fad’ company many try to paint it as years ago.

They have diversified into new brands through the HeyDude acquisition, added forms/styles (in addition to the iconic clogs) such as sandals and jibbitz, and have shown an ability to stay relevant over the years by refreshing the brand and through clever marketing campaigns.

What we perhaps find most interesting is that we view Crocs as transitioning from a one-time type of purchase to a regular fixture on the ‘shoe rack’, alongside your running shoes, boots, slippers, formal shoes and so on.

The i2i Long/Short US Equity Fund holds a financial interest in CROX.

**

Dennis Mitchell, CEO & CIO, Starlight Capital

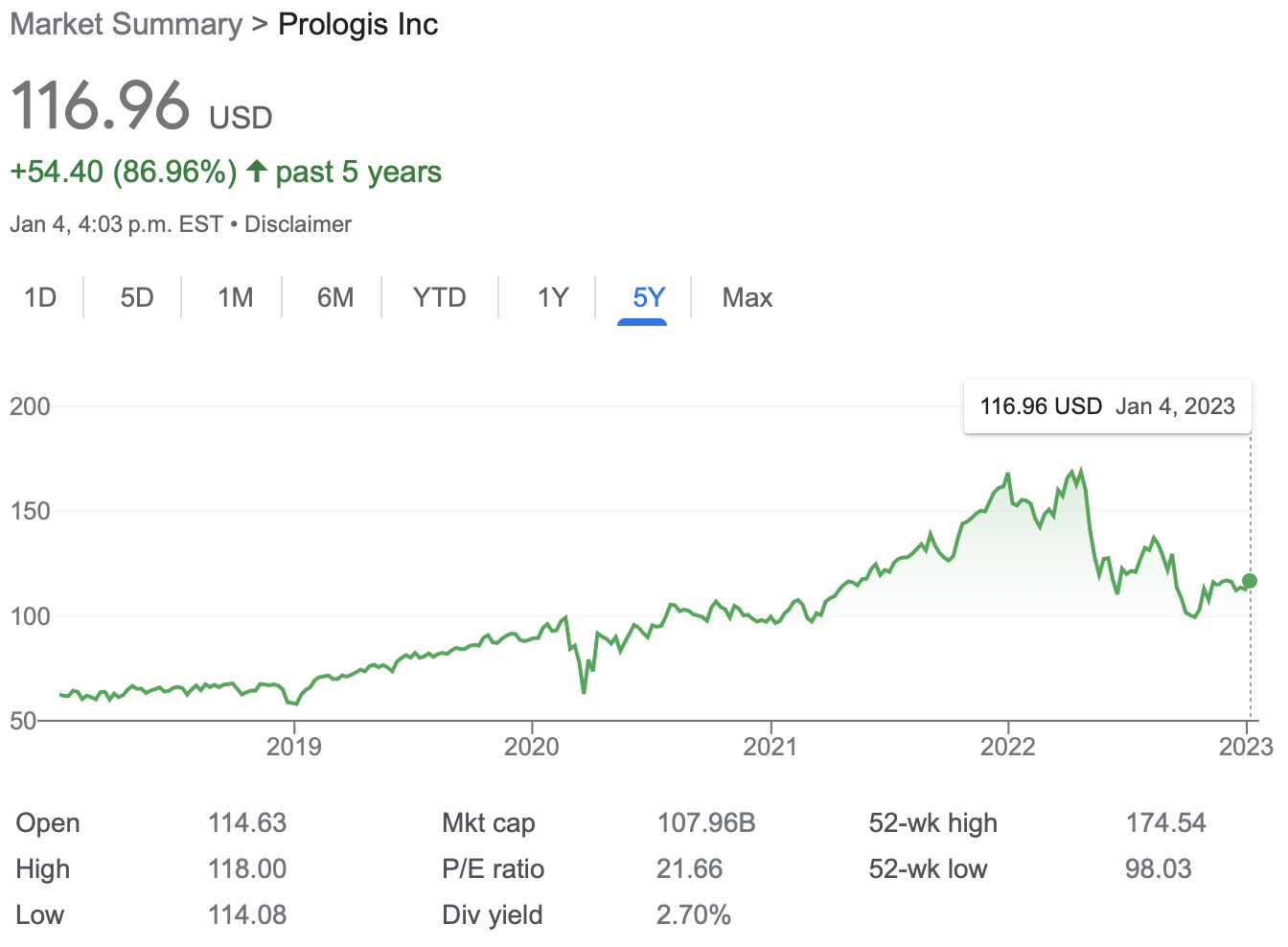

Prologis Inc. (NYSE:PLD)

We like Prologis Inc. as industrial real estate will continue to benefit from the rise of e-commerce and continued consumer spending.

Prologis is the largest industrial REIT in the world but still has significant opportunities to grow.

Prologis offers a 2.7% dividend yield, but the dividend has grown at an 12.4% compound annual growth rate (CAGR) over the last 5 years.

In addition, 15% of Prologis’ leases expire in 2023 at rents that are approximately 60% below market rates.

Prologis trades at a small discount to Net Asset Value despite its very strong balance sheet with a loan-to-value (LTV) ratio of 18%.

Prologis’ development pipeline should deliver $3 billion of new warehouses in 2023 at a 6% yield.

Prologis continues to execute accretive acquisitions, closing on Duke Realty Trust for $23B in 2022.

Prologis’ adjusted funds from operations (AFFO) per share growth is forecast to be 8% in 2023 (up from 6% in 2022), supported by S-P net operating income (NOI) growth of 8%+.

**

Jesse Gamble, Senior VP & Portfolio Manager, Donville Kent Asset Management

Reitmans (TSXV:RET.A; TSXV:RET)

Covid lockdowns proved to be a decisive moment for Reitmans.

Due to government forced store closures, Reitmans strategically entered CCAA protection and restructured their business.

They exited this process in 2022 after:

- Closing over 30% of their stores

- Consolidating their banners from five to three

- Laying off 1,600 employees

- Paying 50 cents on the dollar to settle debt & liabilities

This process gave them cover and a cheaper way to close unprofitable stores and renegotiate retail leases at an opportune time.

We estimate they saved 10% on lease costs across their high-tier locations and over 60% on their second-tier locations.

Now Reitman’s carries:

- $68m of cash

- No debt

- Has reported Net Income of ~$60m in the last 12 months

- Owns roughly $200m of real estate in Montreal

- All while trading at a $110m market cap

Add in a quickly growing e-commerce segment, now representing 25% of sales, positive online search trends, increasing revenue per square foot and decreasing cost per square foot, we think the profitability is sustainable.

In past recessions, like 2001/2002 & 2008/2009, the business remained profitable, as they are a value brand, plus they are one of the few retailers with a growing customer base.

We estimate their target market is growing 3.3% per year.

We think the stock will see a massive re-rating in 2023 as it gets back onto investors’ radars and reinstates dividends & buybacks, plus gets a push to monetize real estate.

**

Josef Schachter, President, Schachter Energy Services Inc.

Pipestone Energy Corp. (TSX:PIPE)

Reasons:

- Pipestone has a market cap over $800 million (M), minimal debt $131M (Q3/22) and production of 32,108 barrels of oil equivalent per day (boe/d), 40% of which is liquids, in Q3/22, up 30% from 24,704 boe/d in Q3/21.

- PIPE sees growth into 2024 (when LNG Canada starts up to 40,000 – 42,000 boe/d. Cash flow should be $380M or $1.34 per share in 2022.

- In 2023 we forecast production rising to 35,000 boe/d and for cash flow to grow to $400M or $1.40 per share.

- PIPE generates free funds flow and will use this to pay down debt further, has recently implemented a dividend of three cents per quarter (4% yield) and may increase dividends, pay special dividends, or have an active normal course issuer bid (NCIB) in 2023.

- Our net asset value (NAV) for PIPE is $7.45 per share, our one-year target is $7.00 per share and our bull market peak target is $12.00.

- PIPE is likely a takeover candidate as the liquids rich Montney play sees further consolidation.

**

Horst Hueniken, President & CIO, Hueniken Asset Management

Legend Power Systems Inc. (TSXV: LPS) is a maker of a patent-protected Active Power Management technology which lowers electricity consumption and the carbon footprint of commercial and residential buildings.

After introducing its third-generation SmartGATE product and customers completing field trials with this technology, the company is at a sales inflection point.

Rather than selling one, two, or five units at a time, from now on, its primary customers will be issuing 100-plus unit, multi-year purchase orders.

The CEO has said, “It is not a question of if, but when [this happens].”

Consequently, bookings are estimated to reach $15 million in 2023 and well beyond in subsequent years.

This exponential sales revenue curve has only begun to be reflected in the company’s valuation, given its break-even sales level is $10 million and its price-to-earnings multiple is six times on our projected 2024 numbers.

**

Matthew Aspro, Investment Analyst, Davis Rea Investment Counsel

Bank of America (NYSE:BAC)

Bank of America is well-positioned to weather the expected modest recession and outperform the market due to:

- A structurally favourable interest rate environment

- Strong household balance sheets

- A track record of delivering attractive shareholder returns

The current strong labour market is a key indicator that there will be a low risk of a sharp increase in loan losses, which will help to maintain a favourable Net Interest Margin (NIM) growth profile for the bank.

Additionally, Bank of America is a leader in technological innovation, investing close to $10 billion per year to drive improvements in the consumer experience and reduce the bank’s operating expenses.

These investments will further strengthen the bank’s position and allow it to continue delivering strong performance in the future.

**

Bruce Campbell, Founder & Portfolio Manager, StoneCastle Investment Management

Rekor Systems Inc (NASDAQ:REKR)

Rekor is a technology company that uses AI to collect, monitor and analyze data for traffic and security solutions.

Rekor is building a recurring revenue model where contracts will be with governments of all sizes.

The company has several data collection trials with multiple state governments across the US.

As these trials are moved to long term contracts Rekor will begin to see high ramp in revenue with strong margins.

Editor’s note: Rekor is also a turnaround story. The stock traded at more than $23 a share in April of 2021.

**

Related stories:

Eight Top Global Stock Ideas for 2023

Contrarian Wins Our 2022 Stock Picking Challenge with Gain of 40%