For a while there it looked like Snap was going to join the ranks of heavyweight apps like Facebook and Instagram.

It’s disappearing photo technology and fun, face-altering features were hugely popular among young teenagers and the sky seemed to be the limit for user growth and eventual profitability.

But Snap has struggled to follow through since going public in March of 2017 as user growth has slowed, profitability remains a dream, and TikTok has bolted past it with an estimated 800 million users compared to about 200 million for Snapchat.

But Snap’s stock price remains stubbornly high suggesting the company is “priced to take over the world’ despite it being an “extremely risky” investment, according to a report by Forbes contributor, David Trainer, of New Constructs LLC:

The following is a condensed version of Trainer’s report:

I first warned investors about SNAP before its IPO in February 2017: Danger Zone: Snap Inc.

I warned again in August 2018, Bursting SNAP’s (Micro) Bubble, before closing the position in February 2019 after the stock had fallen 65 per cent from its IPO closing price while the S&P 500 had increased 14 per cent.

Now, with the stock trading ~155 per cent above where I closed the position, the valuation implies nearly the entire global population will be Snapchat users.

Fiduciaries should consider this stock extremely risky, especially in today’s market. Snap (NASDAQ:SNAP) is this week’s Danger Zone pick.

This report shows investors of all types just how extreme the risk in SNAP is based on:

- Lack of competitive advantages vs. fierce, deep-pocketed competitors

- Growth is with very low-spending (aka unprofitable) users

- Doing the math: the stock price implies Snap’s daily active users (DAU) will equal the world assuming it maintains its current average revenue per user (ARPU). At Facebook’s ARPU, the price implies Snap will reach 11% more daily active users (DAUs) than Facebook.

Growth Will Slow, But Competition for Ad Dollars Will Increase

As the firm attempts to scale up, and more competition enters the market (in some cases directly copying Snap’s core product), it becomes harder to maintain its past growth rates.

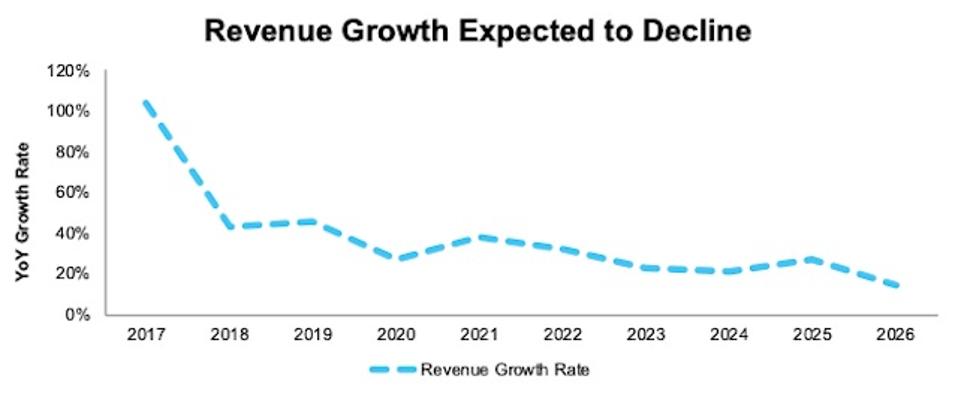

Revenue grew 104 per cent year-over-year in 2017 and 45 per cent in 2019. Consensus estimates expect revenue will grow 27 per cent in 2020, and just 15 per cent by 2026, per Figure 1.

Snap faces an increasingly uphill battle to grow revenue at high rates as the fight for ad dollars intensifies.

Figure 1: Consensus Revenue Growth Estimates: 2017-2026

Growth Focused in Unprofitable Markets

As with most social media companies, the road to profitability, which is elusive for nearly all but Facebook, begins with growing users.

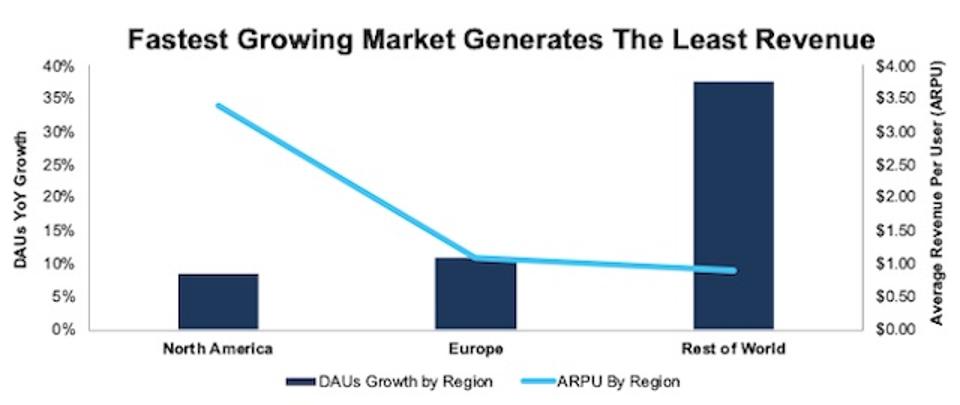

Unfortunately for Snap, and investors that care about profitability, the firm’s growth is coming from its least lucrative market:

“Rest of World.” Snap’s Rest of World DAUs grew 38 per cent in 2Q20, compared to just 11 per cent and 8 per cent for Europe and North America.

Figure 2: DAUs Growth & ARPU by Geographic Region – 2Q20

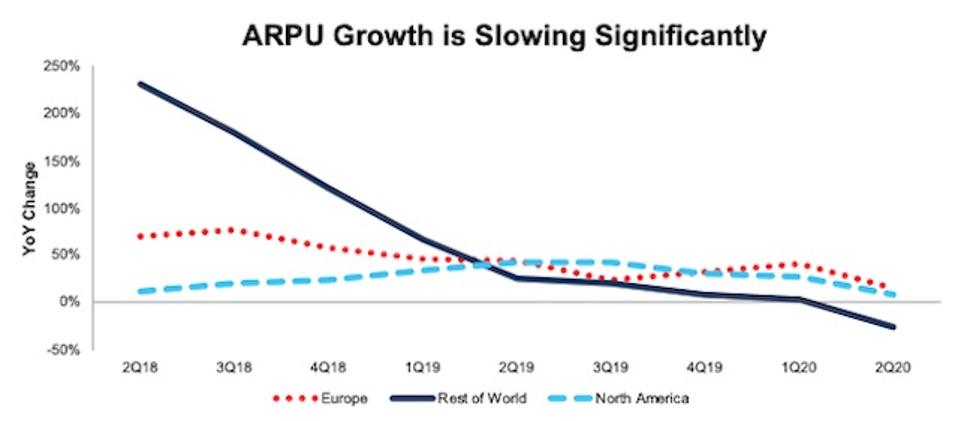

The rate at which Snap is improving its overall ARPU is slowing too, per Figure 3.

Figure 3: YoY ARPU Growth Rates: 2Q18 through 2Q20

Will Snap Ever be Profitable?

With revenue and ARPU growth slowing, it appears Snap’s path to profitability requires a significant reduction in expenses.

I don’t see significant cost reduction coming anytime soon because it signals that the company has given up trying to grow and achieve scale, and that signal would likely cause most investors to sell.

Figure 4: Total Costs & Expenses as a Percent of Revenue: 2018 through TTM

Fierce Competitors

Regardless of user base and growth rates, Snap’s heavy reliance on advertising dollars (98 per cent of revenue in 2019) means it competes with some of the largest, most successful and most profitable media/internet firms in the world.

Snap’s direct competitors include Facebook and Instagram, Alphabet, Twitter, Pinterest, ByteDance (owner of TikTok), and more.

If Snap increases prices for ads, advertisers have plenty of other, larger platforms to spend ad budgets.

Competitive Disadvantages Mean Big Losses

Given the competitive market and negative margins, it should come as no surprise that Snap’s losses are large.

Per Figure 6, Snap has grown revenue by 133 per cent compounded annually since 2015. Snap’s core earnings, which have never been positive, have fallen from -$357 million in 2015 to -$1.1 billion over thew last 12 months.

Figure 6: Revenue Vs. Core Earnings: 2015 through trading 12 months

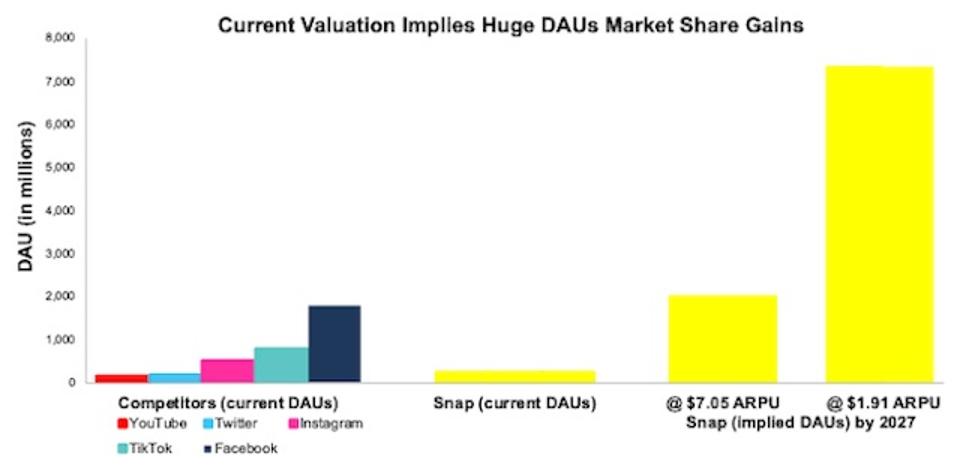

I compare the DAUs implied by Snap’s stock price to some of its largest competitors, per Figure 9. At its current ARPU, Snap’s stock price implies it will have more DAUs than Facebook, TikTok, Instagram, Twitter, and YouTube combined.

Figure 9: SNAP’s Valuation Implies DAUs Will Dwarf Competition

Significant Downside in a More Realistic Scenario

Given the competitive issues discussed so far, I believe the future cash flow scenario above is highly unlikely, if not impossible for Snap to achieve.

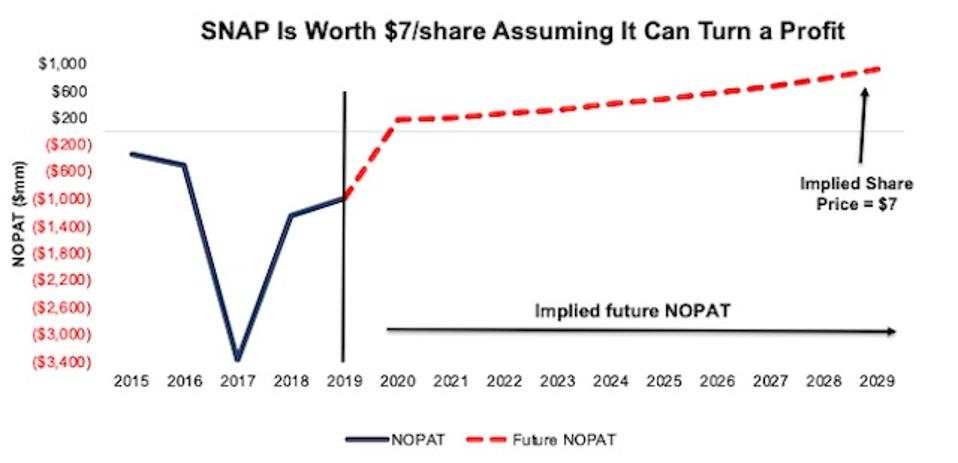

If I assume Snap can achieve an 8 per cent net operating profit after tax (NOPAT) margin and grow revenue by 21 per cent compounded annually for the next decade, the stock is worth only $7/share today – a 70 per cent downside to the current stock price.

Figure 11: Snap Has Large Downside Risk: DCF Valuation Scenario

Insider Are Selling and Short Interest is Notable

Over the past 12 months, insiders have purchased 17 million shares and sold 40 million shares for a net effect of ~23 million shares sold. These sales represent nearly 2 per cent of shares outstanding.

There are currently 73 million shares sold short, which equates to 5 per cent of shares outstanding and nearly three days to cover. The number of shares sold short has declined by 12 per cent since last month, but it’s clear a portion of investors aren’t buying Snap’s story.

Charts: New Constructs, LLC

Related stories: Facebook Changing Free Speech Stance?