Legendary investor Howard Marks has been writing indispensable memos about investing for decades.

He makes them available for free on the Oaktree Capital website.

Marks’ latest examines the investor psychology behind bull and bear markets and how the names, faces, and stocks change over the years, but human nature does not.

That’s why bull market history doesn’t repeat, but often rhymes.

**

by Howard Marks (see below for the full, unedited version of his memo)

While I employ a great many adages and quotes in my writings, my main go-to list consists of a relatively small number.

One of my favourites is widely attributed to Mark Twain:

“History doesn’t repeat itself, but it does rhyme.”

It’s well documented that Twain used the first four words in 1874, but there’s no clear evidence that he ever said the rest.

Many others have said something similar over the years, and in 1965 psychoanalyst Theodor Reik said essentially the same thing in an essay titled “The Unreachables.”

It took him a few more words, but I think his formulation is the best:

There are recurring cycles, ups and downs, but the course of events is essentially the same, with small variations. It has been said that history repeats itself. This is perhaps not quite correct; it merely rhymes.

The events of investment history don’t repeat, but familiar themes do recur, especially behavioural themes. It’s these that I study.

In the last two years, we’ve seen dramatic examples of the ups and downs Reik wrote about.

And I’ve been struck by the reappearance of some classic themes in investor behaviour. They’ll be the topic of this memo.

A bull market shouldn’t be defined as a percentage price movement.

For me, it’s best described by what it feels like, the psychology behind it, and the behaviour that psychology leads to.

If the stock market was a machine, it might be reasonable to expect it to perform consistently over time.

Instead, I think the substantial influence of psychology on investors’ decision-making largely explains the market’s gyrations.

When investors turn highly bullish, they tend to conclude that:

(a) everything’s going to go up forever and

(b) regardless of what they pay for an asset, someone else will come along to buy it from them for more (the “greater-fool theory”).

Bull Market Psychology

In a bull market, favourable developments lead to price rises and lift investor psychology.

- Positive psychology induces aggressive behaviour.

- Aggressive behaviour leads to higher prices.

- Rising prices encourage rosier psychology and further risk-taking.

- This upward spiral is the essence of a bull market.

- When it’s underway, it feels unstoppable.

The most important thing about bull market psychology is that, as cited in the final bullet point above, most people take rising stock prices as a positive sign of things to come.

Many are converted to optimism.

Relatively few suspect that the gains to date might have been excessive and borrowed from future returns and that they presage reversal, not continuation.

That reminds me of another of my favourite adages – one of the first ones I learned, roughly 50 years ago – “the three stages of a bull market”:

- The first, when a few forward-looking people begin to believe things will get better,

- The second, when most investors realize improvement is actually underway, and

- The third, when everyone concludes that things will get better forever.

The bull market of 2020 was unprecedented in my experience, in that there was essentially no first stage and very little of the second.

Many investors went straight from hopeless in late March to highly optimistic later in the year.

This is a great reminder that, while some themes do recur, it’s a big mistake to expect history to repeat exactly.

Bull markets are, by definition, characterized by exuberance, confidence, credulousness, and a willingness to pay high prices for assets – all at levels that are shown in retrospect to have been excessive.

History has generally shown the importance of keeping these things in moderation.

For that reason, the intellectual or emotional rationale for a bull market is often based on something new that history can’t be used to discount.

Those last six words are very important.

I don’t think investors are actually forgetful.

Rather, knowledge of history and the appropriateness of prudence sit on one side of the balance, and the dream of getting rich sits on the other.

The latter always wins.

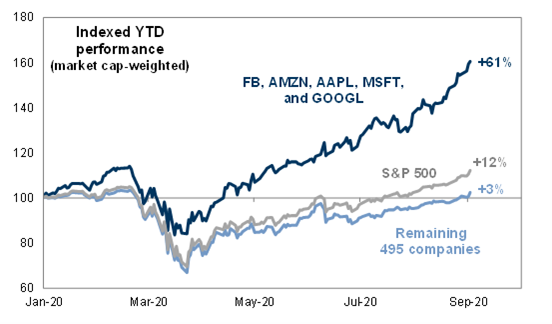

In many bull markets, one or more groups are anointed as what I call “super stocks.”

Topping the list of companies that fed investors’ excitement in 2020-21 were the FAAMGs, whose level of market dominance and ability to scale had never been seen before.

The performance of the super stocks inflamed investors’ ardor, enabling them to disregard worries regarding the persistence of the pandemic or other risks.

Source: Goldman Sachs

Since I’m relying on time-worn investment adages, it’s appropriate at this point to invoke the one I consider the greatest regarding investor behaviour over cycles:

“What the wise man does in the beginning, the fool does in the end.”

When bull markets heat up and good returns encourage investors’ optimism, the traits that are rewarded are eagerness, credulousness, and risk-taking.

In stage three of a bull market, new entrants buy aggressively, keeping it aloft for a while.

Caution, selectivity, and discipline go out the window just when they’re needed most.

Because of all the above, the term “bull market psychology” isn’t a positive.

It connotes carefree behaviour and a high level of risk tolerance, and investors should find it worrisome, not encouraging.

However, the stocks that rise the most in the up years often experience the greatest declines in the down years.

The applicable adages here are from the real world, but that doesn’t reduce their relevance:

“Live by the sword, die by the sword;” “What goes up must come down;” and “The bigger they are, the harder they fall”:

The common thread isn’t fundamentals: it’s psychology, and when the latter changes significantly, all of these things are similarly affected.

The Lessons

As always for students of investing, what matters most isn’t what events transpired in a given period of time, but what we can learn from these events.

And there’s a lot to be learned from the trends in 2020-21 that rhymed with those in previous cycles.

In bull markets:

- Optimism builds around the things that are doing spectacularly well.

- The impact is strongest when the upswing arises from a particularly depressed base in terms of psychology and prices.

- Bull market psychology is accompanied by a lack of worry and a high level of risk tolerance, and thus highly aggressive behaviour.

- Risk-bearing is rewarded, and the need for thorough diligence is ignored.

- High returns reinforce belief in the new, the unlikely, and the optimistic.

- When the crowd becomes convinced of those things’ merit, they tend to conclude “there’s no price too high.”

- These influences cool eventually, after they (and prices) have reached unsustainable levels.

- Elevated markets are vulnerable to exogenous events, like Russia’s invasion of Ukraine.

- The assets that rose the most – and the investors who over-weighted them – often experience painful reversals.

These are themes I’ve seen play out numerous times during my career.

None of them relates exclusively to fundamental developments.

Rather, their causes are largely psychological, and the way psychology works is unlikely to change.

That’s why I’m sure that as long as humans are involved in the investment process, we’ll see them recur time and time again.

And, as a reminder, since the major ups and downs of the markets are primarily driven by psychology, it’s clear that market movements can only be predicted, if ever, when prices are at absurd highs or lows.

Here’s the full version of Marks’ memo.

**

Related stories: When to Sell: Excerpts from Howard Marks’ Latest Memo