When we interviewed Dr. Ed Yardeni in late October of 2022, he told us he believed there were “tremendous opportunities” in the stock market despite what he called a “rolling recession” in the U.S.

Now, the President of Yardeni Research believes that rolling recession may be turning into a “rolling expansion” based on some of the economic data released this past week.

Since Yardeni’s comments about nine months ago during our conversation, the S&P 500 is higher by nearly 20%.

Nice call, Dr. Ed.

This performance despite a lot of negative economic data and doom and gloom headlines in the financial media.

What are the economic data points that have Yardeni suggesting the economy is better shape than many people think?

In one of his QuickTakes reports this week, Yardeni isolated five economic reports that indicate to him the “permabears will have to postpone their imminent recession yet again” as the economy shifts into a rolling expansion.

See Yardeni’s commentary below accompanied by five illuminating charts.

**

by Ed Yardeni

The permabears will have to postpone their imminent recession yet again based on today’s batch of US economic indicators, which suggests that our “rolling recession” is turning into a “rolling expansion.”

The housing market seems to be recovering nicely from its recession, which started early last year.

The manufacturing sector is showing signs of bottoming, while nondefense capital goods orders excluding aircraft rose to a record high in May.

Consumer confidence is improving, as job openings remain plentiful.

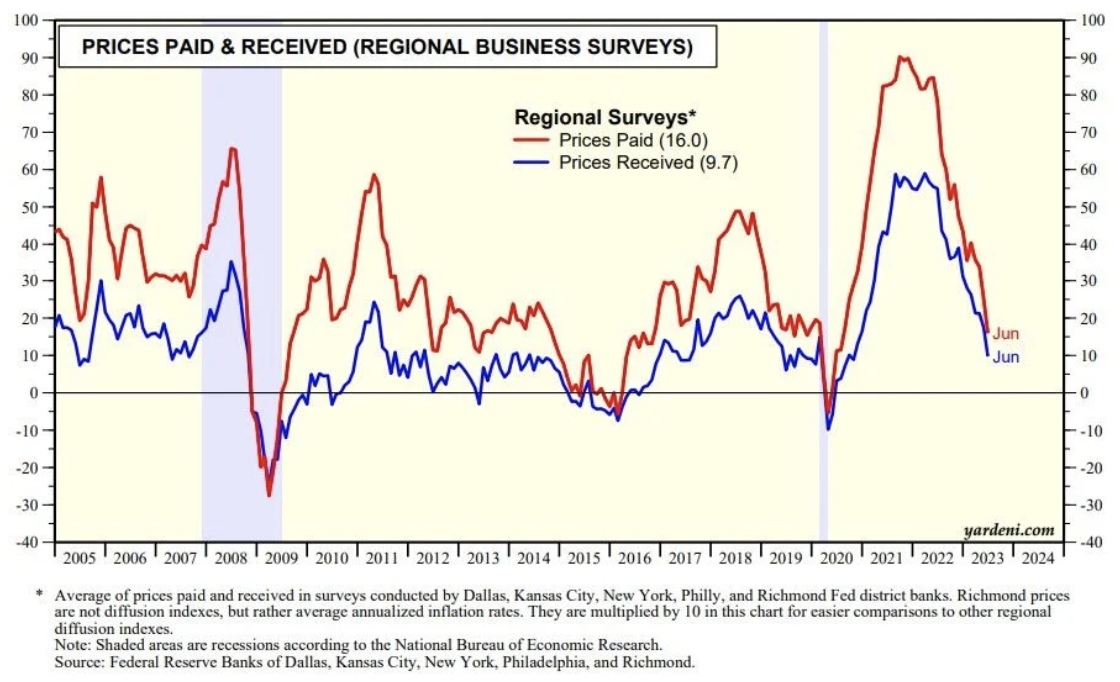

Notwithstanding all these upbeat developments for the economy, regional surveys of prices paid and received remain disinflationary.

It all supports our rolling-expansion-with-disinflation (REWD) scenario.

And support for REWD confirms RRWD—the rolling-recession-with-disinflation outlook we have held since early last year.

The stock and bond markets seem to share our optimism about the fundamentals.

Consider the following:

(1) New home sales soared during May (chart).

Builders are scrambling to build more inventory to satisfy pent-up demand.

New home sales are reaching levels seen before the pandemic.

(2) The average of the general business indexes of the regional business surveys conducted by five of the 12 Federal Reserve district banks jumped in June, suggesting that the manufacturing recession may be bottoming (chart).

(3) New orders for manufactured goods jumped 1.7% month-over-month (m/m) in May and rose for the third month in a row, boosted by strong demand for passenger planes and new autos.

Business investment also increased.

Nondefense capital goods orders rose to a record high in May (chart).

(4) The Conference Board said its consumer confidence index (CCI) rose to 109.7 this month, the highest reading since January 2022.

The survey used to calculate the CCI showed that the “jobs plentiful” series remained high in June at 46.8% (chart).

(5) Topping off the milk-and-honey batch of indicators today, the June averages of the prices-paid and prices-received indexes based on the regional business surveys conducted by the five Federal Reserve district banks showed that inflationary pressures continue to subside rapidly (chart).

You can subscribe to QuickTakes here.

**

Related stories: “Tremendous Opportunities” for Investors Despite “Rolling Recession.” – Ed Yardeni Interview

“Roaring ’20s” Still Possible After “Mother of All Meltups” & Meltdown – Ed Yardeni Interview