Jeremy Grantham was right.

The legendary investor, bubble historian and Long-Term Investment Strategist and Co-Founder of GMO, wrote about a year ago that the stock market “super-bubble” was starting to unwind.

His confidence came from studying what he considers the largest super-bubbles of modern times ( excluding tulips and a few other manias), 1929, 2000, U.S. housing in 2007, the dual real estate and market bubbles in Japan in 1989, and the multiple super-bubbles that peaked around November of 2021.

Grantham says these manias all have similar characteristics in part because human behaviour doesn’t change too much.

Here are the hi-lights of Grantham’s most recent letter to clients in which he explains that the first leg of the super-bubble unwind is mostly complete.

But now things get more complicated.

Executive Summary

The first and easiest leg of the bursting of the bubble we called for a year ago is complete.

The most speculative growth stocks that led the market on the way up have been crushed, and a large chunk of the total losses across markets that we expected to see a year ago have already occurred.

Given the starting conditions of extraordinary speculative euphoria, this was all but certain.

The negative surprises of last year, from war in Ukraine to the global inflation spike, were quite unnecessary to ensure a significant downturn.

Now things get more complicated.

While the most extreme froth has been wiped off the market, valuations are still nowhere near their long-term averages.

Further, in the past, they have usually overcorrected to below trend as fundamentals deteriorated.

Such an outcome still remains highly likely, but given the complexities of an ever-changing world, investors should have far less certainty about the timing and extent of the next leg down from here.

In fact, a variety of factors – especially the underrecognized and powerful Presidential Cycle, but also including subsiding inflation, the ongoing strength of the labor market, and the reopening of the Chinese economy – speak for the possibility of a pause or delay in the bear market.

How significantly corporate fundamentals deteriorate will mean everything during the next twelve to eighteen months.

Beyond the near term, for long-horizon fundamental investors, the biggest picture remains that long-run issues of declining population, raw materials shortages, and rising damage from climate change are beginning to bite hard into growth prospects.

The resource and geopolitical shocks of last year will only exacerbate those issues.

And over the next few years, given the change in the interest rate environment, the possibility of a downturn in global property markets poses frightening risks to the economy.

The January Rally

The recent rally brings up another embarrassingly simple factor, the January effect.

January features relative strength in characteristics beloved of individuals.

Institutions love large capitalization and quality, and these characteristics provably outperform their beta for the remaining 11 months.

But historically individuals prefer small caps, stocks that are obviously cheap, and confusingly, stocks that got hammered the year before.

The latter presumably because they have just finished tax loss selling and have that money in hand – plus any year-end bonuses and distributions.

Additionally, this year they still have the balance of the stimulus money.

So you might have guessed that the bounce in the previous year’s speculative losers might be powerful this year.

I read about the recent 20% rally in Bitcoin and friends, which was allegedly for exotic reasons.

More likely to me this is merely crypto’s usual style of behaving like the most speculative stocks, almost all of which had a terrible 2022.

This type of rally after a bloodbath is not unusual and may very well not outlive January.

But it is yet one more factor that may help postpone the market lows for a while.

PS – Investing in a Particularly Tricky World

Despite the generally unattractive nature of the U.S. equity market and the extremely tricky global economy, there are still a surprising number of reasonable investment opportunities even if they are not sensational.

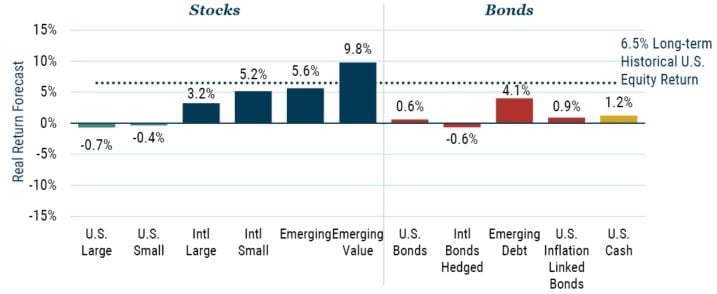

Exhibit 4 is GMO’s 7-Year Asset Class Forecast.

It shows that emerging markets are reasonably priced and the value sector of emerging is cheap.

Admittedly they came into this broad decline a year ago much cheaper than the U.S. yet have gone down similarly.

This is disappointing but quite typical.

The first phase of a bear market typically is a broad markdown with only generalizations used for differentiation.

Subtleties of relative value are left for later.

My favorite example was 2002, the third year of the great tech bust, in which the S&P 500 was down 22% and the highest beta, but much cheaper, emerging equities were down only 2%!

EXHIBIT 4: GMO 7-YEAR ASSET CLASS FORECASTS*

Full version of Grantham’s letter

**

Related stories: Bubble Spotter Grantham on What To Do As “Wild Rumpus” Begins