Germany this week technically fell into recession with two consecutive quarters of GDP contraction.

It’s been the consensus for a long while that the U.S. will eventually do the same.

After all, most of the economic data, with the exception of resilient employment numbers, indicates that will be the case.

Or does it?

The major stock indices continue to rise and we haven’t seen a flight to the safety of government bonds.

Is it possible that economic growth and corporate earnings have already troughed and that the stock market has it right in front running a pause on interest rate hikes by the U.S. Federal Reserve and eventual rate cuts?

That forms part of the argument in a report from an independent, macroeconomic strategy team.

We present the highlights here, including some intriguing charts.

by Alpine Macro

On the surface, the case for a recession seems to be both straightforward and ironclad:

- A deeply inverted Treasury yield curve signals that the Fed has over-tightened;

- A steep drop in oil prices suggests waning demand;

- Tightening lending standards will choke business activity and M2 (money supply) contraction, rare in U.S. history, could signal a sagging economy.

Meanwhile, credit demand has slumped in response to higher rates.

The regional banking crisis will make the crunch even worse, particularly for small businesses who are most dependent on this channel of credit access.

Historically, sagging loan demand and tightening lending standards only happen either a few months before or during recessions (Chart 1).

In other words, the U.S. economy should be in a recession now.

Yet, first-quarter S&P 500 earnings have surprised to the upside, with 78% of companies having beaten market expectations (Chart 2).

Counterintuitively, Chart 3 shows that after an 18% drawdown last year, operating EPS appear to have bottomed out in Q4 2022, while earnings expectations are now rising anew.

We believe that the stock market has got the earnings story right.

Yes, the cumulative impact of the Fed’s monetary tightening will be weak or declining real economic output, but relatively high inflation may also offer some protection to nominal earnings.

The big difference between today’s economic environment and the pre-pandemic period is that inflation, though falling, remains significantly higher than at any time since the 1990s.

This will likely have an impact on how the economy responds to various policy shocks.

Importantly, nominal GDP growth usually stays positive, even when the U.S. economy enters recession.

For example, throughout the 1970s and 1980s, nominal GDP growth averaged 4-5% when the economy went through deep recessions.

Corporate revenue and profits are nominal variables, and intuitively, rising prices should help rather than hurt corporate profitability.

From a macro perspective, nominal GDP is indeed a close proxy for corporate revenues (Chart 4).

Nevertheless, this does not change the fact that strong pricing power helps corporate profitability.

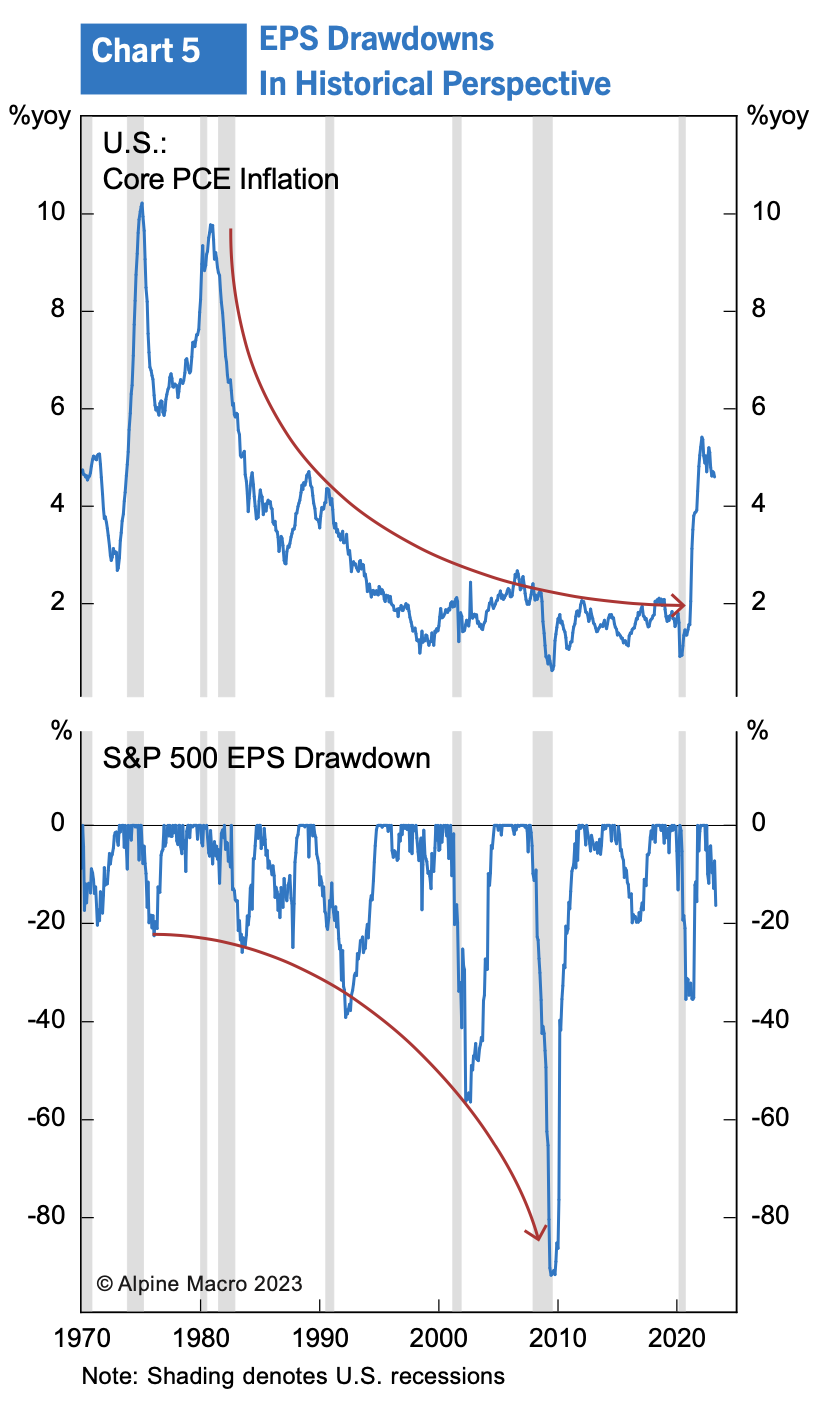

Chart 5 shows that recessions in the 1970 and 1980s were severe, but EPS drawdowns were much milder than those in recent decades when low inflation prevailed.

For example, the average decline in EPS was 21% in the 1970s and 1980s.

Perhaps the stock market has figured out that even if the economy falls into a mild recession (defined as two consecutive quarters of negative real output growth), elevated pricing power will still largely bail out EPS growth.

In other words, we may have a combination of disinflation, mild recession, positive earnings growth, and rising stock prices, the equivalent of “having your cake and eating it too”.

There is also possibility that, while most in the investment community expects a sharp drop in profits, an earnings recession has already taken place.

The U.S. economy has slowed sharply since late 2021, including two consecutive quarters of GDP contraction in the first half of 2022, so technically the U.S. economy experienced a recession.

During this period, operating EPS for the broad index contracted 18% from its cyclical highs, while stock prices fell by 25% before reaching a bottom last October (Chart 7).

Importantly, the total drawdown in EPS last year was comparable with recessions in the 1970s.

In the 1970s and 1980s, however, economic shocks were mostly inflationary in nature, and therefore the Fed’s core objective was to quash excess demand by raising rates to cool inflationary pressures.

Once the tightening cycle stopped and reversed, the economy and stocks tended to rebound quickly.

As far as the recent cycle is concerned, the Fed is clearly dealing with a big inflation shock similar to the 1970s, which is the key reason that the correlation between equity prices and interest rates has turned negative.

The only difference is that the market has become much more anticipatory than before, such that risk asset prices are front running changes in Fed policy.

Therefore, even if the Fed is expected to go on hold, it represents a positive change for the stock market.